Why National Insurance rejected TP claim is the last thing you want to Google after an accident, but it is exactly when you need clear guidance.

In this guide I will explain, in plain English and from an ex-NICL employee’s view, what “driver at fault” and “no FIR” actually mean for your third party claim and how to fight an unfair rejection in 2026.

How Third Party Claims With National Insurance Actually Work

When people ask why National Insurance rejected TP claim, most of them are not clear about what third party cover really pays for. Third party motor insurance is a statutory cover under the Motor Vehicles Act to protect victims, not to protect the negligent insurer or the wrongdoer.

National Insurance, like any other insurer, collects TP premium and then has a legal duty to pay awards ordered by the Motor Accident Claims Tribunal (MACT) when liability is established. It cannot arbitrarily cancel statutory TP cover except in very narrow situations like double insurance or total loss of the vehicle.

TP cover vs own damage – what National Insurance is liable for

Many policyholders confuse TP claims with own damage claims and then cannot understand why National Insurance rejected TP claim citing “driver at fault”. In simple terms:

- Third party cover pays compensation to the victim of the accident, not to the owner of the insured vehicle.

- Own damage section pays for repairs or total loss of your own vehicle when covered per policy terms.

Even if the driver of the insured vehicle is at fault, TP cover usually still responds towards the injured third party or legal heirs, subject to policy conditions like valid licence and permit. The insurer can later recover from the owner/driver in specific breach situations but cannot casually deny genuine TP liability.

Role of FIR, MLC and police papers in TP claims

A common reason you hear for why National Insurance rejected TP claim is “no FIR, so we cannot process the claim”. In practice, FIR and police papers are important, but they are not the only way to prove an accident.

FIR helps show:

- Date, time and place of accident.

- Vehicles and parties involved.

- Prima facie negligence noted by police.

However, IRDAI’s 2024–26 framework is moving towards “no claim rejection for want of documents” and requires insurers to ask for essential documents at underwriting and only those directly linked to the claim later. For low-value motor losses under a threshold, surveyors may not even be mandatory, and app-based or AI-based assessment is permitted.

So while lack of FIR may complicate liability assessment, it is not an automatic, legal death sentence for every TP claim.

Real Reasons National Insurance Rejects TP Claims as “Driver at Fault”

From the inside, when I saw why National Insurance rejected TP claim in TP portfolios, “driver at fault” was rarely the only reason. It was usually a shorthand for a mix of factors, some valid and some shaky, depending on documentation and legal advice.

No FIR or delayed FIR – Does it legally kill the claim?

Insurers sometimes treat “no FIR” as a convenient reason to slow down or question a TP case, especially when facts are disputed or there is suspected fraud.

But consumer complaints and legal commentary show that courts focus on whether the accident and negligence can be proved overall, not only via FIR.

A delayed FIR, or even no FIR, can be supplemented by:

- Hospital MLC, treatment records and discharge summary.

- Eyewitness statements and photographs.

- Vehicle damage report and site inspection.

IRDAI’s master circular clearly says that no motor insurance claim can be rejected only because some documents are missing if the essential facts are still provable and the insurer had earlier chances to obtain them.

So if you were told National Insurance rejected TP claim only due to “no FIR”, you have a strong ground to appeal.

Licence, drunk driving, permit and other breach issues

The more serious reasons behind “driver at fault” often involve breaches, such as:

- No valid driving licence or expired licence at the time of accident.

- Drunk driving or driving under influence of drugs.

- Vehicle used for hire or reward without required permit.

- Gross negligence like racing or deliberate act.

National Consumer Commission decisions have upheld claim repudiations where the driver had no valid licence, and such breach was treated as fundamental and directly linked to the accident.

In those cases, tribunals sometimes still protect the third party by directing payment by the insurer with a right to recover from the owner, but that depends on facts and pleadings.

So when you get a note that National Insurance rejected TP claim saying “driver at fault”, read whether they are actually alleging a serious policy breach, or casually blaming the driver without strong evidence.

Step-by-Step: What To Do Immediately After TP Claim Rejection

If you woke up to a letter saying National Insurance rejected TP claim, do not panic and do not ignore timelines. Your first job is to understand the exact grounds and gather counter-evidence, not to argue emotionally over the phone. For more templates and wording ideas, you can also refer to this how to appeal a rejected National Insurance car claim guide.

How to read and reply to the repudiation letter

Every rejection letter must clearly state reasons for repudiation and reference the specific policy clauses relied upon. Many letters simply mention “driver at fault” and “no FIR” without connecting them to any exclusion, which is a weak ground under fair practice guidelines.

Do this in order:

- Step 1: Highlight all reasons given, word by word, including any mention of “no FIR” or “late intimation”.

- Step 2: Collect your documents – policy, claim intimation number, RC, DL, permit, hospital papers, photographs, any police GD or NCR. If you are unable to retrieve your e-policy or see errors on the portal, use this guide to fix National Insurance policy download or invalid policy number issues before you proceed.

- Step 3: Draft a written reply to the Branch Manager/Claims Manager, point-wise rebutting each reason with facts and documents.

Many policyholder-side lawyers use a standard template where they call out arbitrary and baseless reasons that are not supported by law or policy terms. You can adapt this approach, but keep the tone factual and firm, not abusive.

Escalation ladder – from branch grievance to Ombudsman

If your written reply does not resolve the issue, escalate formally through the grievance mechanism rather than shouting at the counter. IRDAI’s rules require every insurer to have a structured grievance redressal system and clear turnaround times.

Typical escalation ladder:

- First level: Branch or Divisional Office Grievance Cell (written complaint, acknowledgment within a few days – you can find your nearest National Insurance branch office details with address, phone and email here)

- Second level: Company Grievance Redressal Officer at Regional or Head Office if you are unsatisfied or get no response in 15–30 days.

- Third level: Insurance Ombudsman in your region for disputes within current monetary limits, with a written award after hearing both sides.

- Parallel track: You can also take the matter to Consumer Commission or MACT through a lawyer, where many unfair repudiations have been overturned.

Use email plus registered post so that you have proof of timelines. This record becomes invaluable if you later pursue the matter before an Ombudsman or tribunal, and you can mirror the sample structure shown in the how to appeal a rejected National Insurance car claim guide.

Can National Insurance Reject TP Claim Without FIR Under 2024–26 IRDAI Rules?

As of 2024–26, regulators have become far stricter about arbitrary motor claim rejection, especially for statutory third party cover. IRDAI’s master circular on general insurance and later communications emphasise speed, fairness, and no rejection merely for “want of documents”.

What IRDAI master circular says on documents and fairness

The master circular states that no motor claim should be rejected just because some documents are unavailable, and that insurers must ask for necessary documents during underwriting. Later, they may ask only for additional papers directly related to the claim like filled claim form, driving licence, permit and basic accident proof.

For motor insurance:

- Timelines are specified for surveyor appointment, survey report and claim decision.

- Board-approved claims policy and transparent deduction rules are mandatory.

- Small losses under a set limit do not always require survey, with app-based assessments becoming common.

In this environment, a blanket statement that National Insurance rejected TP claim “without FIR” and without exploring alternative evidence could be treated as unfair and challengeable before regulators or courts.

When “driver at fault” is not a valid excuse for TP claims

Third party insurance is meant to respond even when the insured driver is negligent; that is precisely why victims are compensated. Blaming the driver for being at fault, by itself, does not let the insurer escape TP liability.

The insurer can legally resist or limit liability when:

- The policy itself is not in force.

- There is a strong, provable breach like no licence, fake licence, or unauthorized use that caused the accident.

- The claim is fraudulent, staged or involves deliberate self-injury or collusion.

If your policy has already lapsed, you should immediately renew National Insurance car insurance policy online to avoid future TP disputes and gaps in cover, even while you contest the current rejection.

If you see that National Insurance rejected TP claim mainly by saying “your driver was at fault” without linking it to a specific exclusion, this is a red flag. Under the current framework, such reasons can be tested against IRDAI’s fairness and transparency standards and may be set aside.

As an Ex-NICL Employee: Insider Tips to Avoid TP Rejection

When I handled motor claims inside a public sector setup, I saw two types of files: those that sailed through because basics were done right, and those that became messy purely due to avoidable mistakes. You can dramatically reduce the risk that National Insurance rejected TP claim for technical grounds if you handle the first 7–10 days correctly.

Checklists for policyholders, drivers and fleet owners

Use this simple checklist whenever a vehicle insured with National Insurance is involved in an accident:

- Ensure immediate medical help first – preserve hospital records and bills.

- Inform the nearest police station; even a GD entry or NCR is better than nothing if FIR is not possible.

- Notify the National Insurance office or call centre within the timelines specified in your policy and claim guide.

- Preserve dashcam footage, CCTV clips, and photographs of the site, vehicles and injuries.

- Keep copies of DL, RC, permit and fitness ready; many rejections stem from missing or invalid documents.

Following this checklist makes it much harder for any insurer to later say they rejected TP claim because “facts were not proved” or “documents were not supplied in time”.

What not to do after an accident

Some actions almost invite trouble and later become the hidden reason why National Insurance rejected TP claim, even if they are not clearly written in the repudiation letter. Avoid these as much as possible:

- Do not run away from the spot without informing police; this often looks like hit-and-run or guilt.

- Do not sign blank forms or statements at workshops or tout offices.

- Do not delay claim intimation for weeks; even under liberal rules, unexplained delay raises suspicion.

- Do not tamper with the vehicle before initial inspection unless safety demands moving it.

When in doubt, speak to a neutral legal expert rather than only relying on cashless workshop advisors, who often focus more on own damage than third party liabilities. If you still prefer cashless repairs, first check the official National Insurance cashless garages list and claim process, so you are not misled about what TP cover actually does.

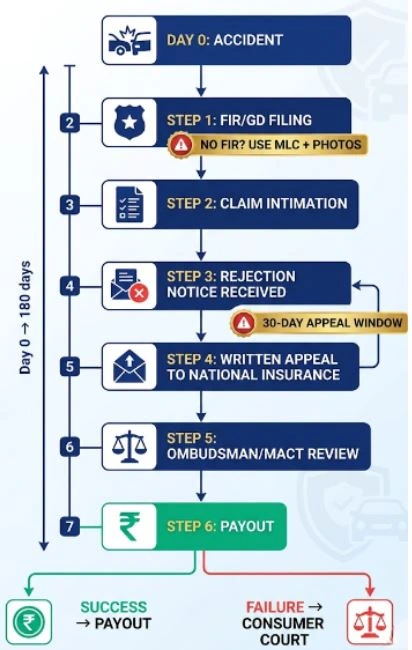

Sample Timeline: From Accident to Final TP Payout in 2026

To understand why National Insurance rejected TP claim in some cases and settled smoothly in others, you must visualize the entire lifecycle of a third party case. Think of it as a 90–180 day journey, sometimes longer if MACT litigation is involved.

Practical 90–180 day flow in plain language

A typical timeline for a straightforward TP bodily injury case may look like this:

- Day 0–1: Accident occurs, medical aid and basic police intimation are done.

- Day 1–3: Claim intimation to National Insurance with policy and vehicle details, initial photos and contact numbers.

- Day 3–15: Insurer appoints surveyor or investigator, gathers police and hospital documents, and may contact witnesses.

- Day 15–60: Liability assessment, negotiation with claimant or handling of legal notices begins.

- Day 60–180: For MACT cases, insurer deposits or pays as per award order, subject to any appeals.

When this flow is followed and both sides cooperate, there is little room for arbitrary reasons like “driver at fault” to derail genuine TP claims. Rejections often appear when evidence is thin, timelines are broken, or serious policy breaches surface late.

2026 Updates: Faster TP Settlements and No-Arbitrary Rejection Rules

From 2024 onwards, IRDAI has issued a series of reforms to make motor claims faster and more transparent, which directly impacts how and when National Insurance rejected TP claim can be justified. These reforms cover timelines, documentation, and prohibited practices.

Key highlights relevant to your TP issue:

- Insurers must publish clear claim settlement turnaround times and follow them.

- “No claim shall be rejected for want of documents” – essential papers must be sought at proposal stage.

- Statutory TP policies cannot be cancelled except in limited circumstances like double insurance or total loss.

- Losses below a certain threshold do not need traditional survey, enabling quicker app-based assessment.

For you, this means any decision where National Insurance rejected TP claim purely due to “no FIR” or vague “driver at fault” must be tested against these guidelines. If it appears arbitrary or unsupported, escalation to Ombudsman or court is not only possible, but often effective.

Call To Action: How I Can Help You Draft a Strong TP Appeal

If you are stuck because National Insurance rejected TP claim citing “driver at fault” without FIR, do not close the file and move on. You still have practical options.

- First, collect your policy, repudiation letter and all accident documents in a single folder.

- Second, draft a structured representation citing IRDAI rules and pointing out where the rejection is vague or contrary to guidelines. You can then send it to the branch and also escalate through the official National Insurance customer care number and email for claims so that your grievance is formally tracked.

- Third, if you want, you can use this article as a checklist while discussing your case with a lawyer or insurance advisor so you do not miss any critical point.

If you share the exact reasons mentioned in your rejection letter, I can help you shape a point-wise rebuttal that speaks the same language claims managers and Ombudsmen understand.

Conclusion:

When you look closely, “why National Insurance rejected TP claim saying driver at fault without FIR” is not just about one accident. It is about how documentation, policy conditions and 2024–26 IRDAI rules interact in real life.

FIR is helpful but not always decisive, driver negligence is expected in TP cases, and arbitrary rejections are increasingly frowned upon by regulators and courts. If you combine timely intimation, proper evidence and a structured appeal, many weak rejections can be challenged successfully.

If you are comfortable sharing, what exact wording has National Insurance used in your TP rejection letter?

FIR is not legally compulsory for every third party claim, although it is a strong piece of evidence to prove that an accident occurred and to show basic details like date, time and parties involved. In many cases, especially minor injuries or property damage, insurers and courts may accept other evidence such as medical records, photographs and witness statements if a FIR could not be filed for valid reasons.

No, simply stating that the driver was at fault does not, by itself, allow National Insurance to escape statutory third party liability. Third party cover is designed to respond when the insured driver is negligent, and the insurer must point to a concrete policy breach or legal defence, such as no valid licence or proven fraud, before refusing to pay.

Your complaint to the Insurance Ombudsman should attach the policy, claim documents, repudiation letter, and a clear explanation of why you believe the rejection is unfair or contrary to IRDAI rules. It helps to highlight any vague or unsupported reasons, such as rejection for want of documents or generic blame on the driver, and to show the steps you took to cooperate with the insurer before escalation.

New IRDAI guidelines mandate that motor insurers have transparent, board-approved claim policies, adhere to defined timelines and avoid rejecting claims solely for lack of documents that should have been collected earlier. They also restrict cancellation of statutory third party policies and encourage the use of technology for faster assessments, making it harder to hide behind vague or technical grounds when denying genuine claims.

Yes, you can still pursue a Motor Accident Claims Tribunal case even if your insurer has denied the claim, because the tribunal independently assesses negligence and compensation based on evidence. The insurer’s repudiation is not final in law, and tribunals sometimes direct insurers to pay the award to the victim with liberty to recover from the owner if a serious policy breach, such as no licence, is proved.

While exact timelines can vary, insurers are generally expected to respond to grievances within a defined period, and the Insurance Ombudsman typically entertains complaints filed within a specified time from the final reply or rejection. It is safer to raise your dispute in writing as soon as possible after receiving the repudiation letter so that limitation does not become a new obstacle later.

If the offending vehicle does not have valid third party insurance, the victim can still claim compensation from the vehicle owner and driver through MACT, but the financial burden falls directly on them. That is why regulators repeatedly stress that third party insurance is mandatory and highlight the legal and financial consequences when more than half of vehicles in India run without valid TP cover.